In the digital age, managing finances has become more convenient than ever. One such app that has revolutionized the way we handle money is Cash App. Developed by Square Inc., Cash App offers a quick and easy way to send, receive, and save money. However, it’s not the only player in the game. There are numerous other apps like Cash App that offer similar, and sometimes even more diverse, features. Let’s explore the top 10 alternatives to Cash App.

Introduction

Cash App, developed by Square Inc., is a mobile payment service that has quickly become a household name in the world of peer-to-peer transactions. It’s like having a digital wallet that’s always with you, ready to make payments or receive funds at a moment’s notice.

With Cash App, you can send and receive money instantly, making it perfect for splitting bills, paying your friends back, or even paying rent. The app is designed to be simple and user-friendly, with a clean interface that makes it easy to enter payment amounts and select recipients.

A list of the Top 10 alternative apps to Cash App

| App Name | Best Feature | Rating | Reviews | Download |

|---|---|---|---|---|

| PayPal | Widely accepted, diverse functionality | 4.8 | 6,180,477 |   |

| Venmo | Social payment app, easy to use | 4.9 | 15,353,331 | |

| Zelle | Direct bank-to-bank transfers | 4.8 | 465,944 | |

| Google Pay | Integrated with Google services | NA | NA | |

| Apple Pay | Seamless integration with Apple devices | NA | NA | |

| Revolut | Avoids costly currency conversion fees | 4.7 | 35,036 | |

| Wise (Formerly TransferWise) | Low-cost international transfers | 4.6 | 28,545 | |

| N26 | Full control over finances, mobile bank | 4.6 | 8,218 | |

| Payoneer | Supports over 150 currencies | 4.5 | 1,820 | |

| Cheese | Offers perks like cashback and early paycheck access | 4.6 | 1,667 | |

Top Apps like Cash App

PayPal

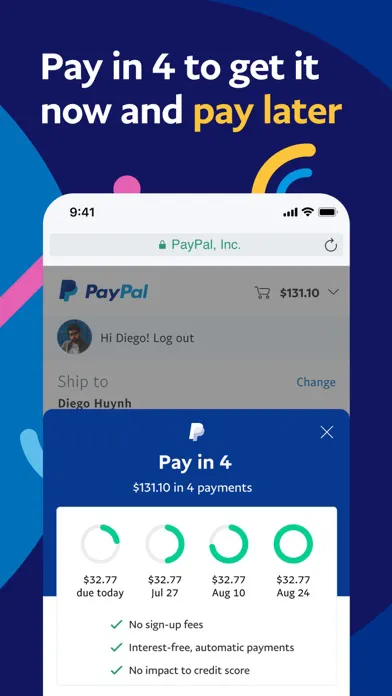

PayPal, developed by PayPal Holdings, Inc., is a global online payment system that has been around for quite some time. It’s like the granddaddy of digital wallets. With PayPal, you can send money to people in more than 100 countries using just their email address or mobile number. On the flip side, you can also receive funds from others directly into your PayPal account. The money can then be transferred to your bank account, or you can use it to buy goods and services from any merchant that accepts PayPal – which is a lot of them! However, some users have reported that PayPal’s customer service can be slow to respond. Despite this, its robust features and global acceptance make it a strong contender in the digital payment space.

Key Features:

- Widespread Acceptance: PayPal is accepted by millions of businesses worldwide, making it a versatile choice for online shopping.

- Money Pool: This feature allows users to create a shared pot of money, making it perfect for group gifts or shared expenses.

- Fees: While sending money domestically is free, there are fees for international transactions and receiving money for goods and services.

Drawbacks:

However, some users have reported that PayPal’s customer service can be slow to respond. Despite this, its robust features and global acceptance make it a strong contender in the digital payment space.

|  |  |  |  |

Venmo

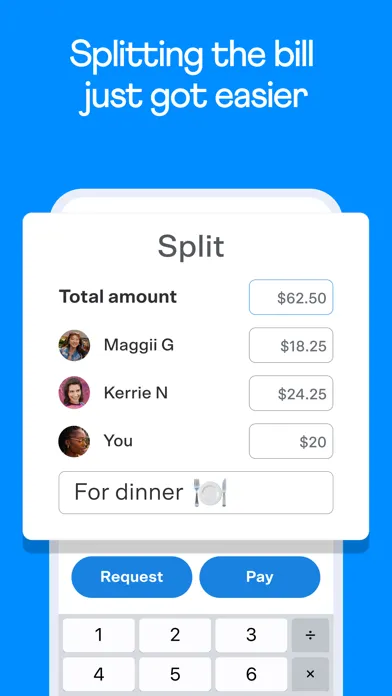

Venmo, a service of PayPal, Inc., is a social payment app that has gained popularity among the younger demographic. It’s like the hip younger sibling of PayPal. Venmo is unique because it combines social networking with financial transactions. You can add a note or even an emoji to each payment you make, and if you want, you can share your transaction with your friends or the public. It’s a fun way to split the bill at a restaurant, pay your roommate for your share of the rent, or chip in for a friend’s birthday gift. However, Venmo charges a 3% fee when you send money using a credit card. Also, its social aspect might not appeal to everyone.

Key Features:

- Social Feed: Venmo includes a social aspect where you can share and view payment descriptions on a public feed.

- Splitting Payments: This feature allows users to split bills and other expenses easily.

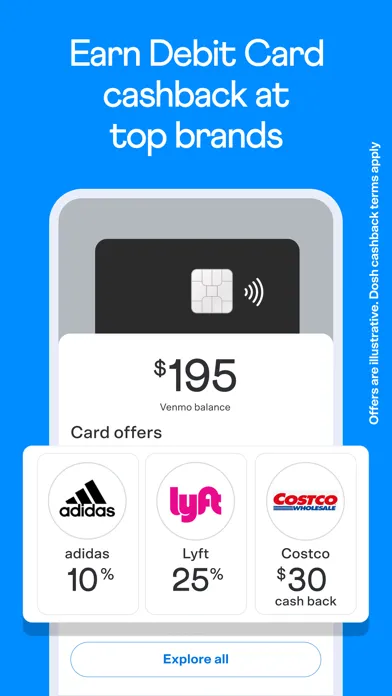

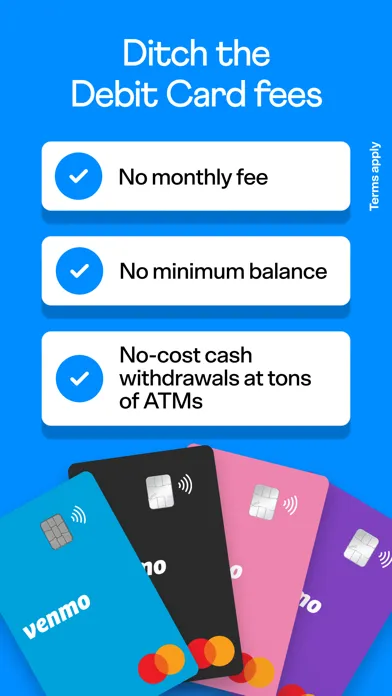

- Venmo Debit Card: Users can apply for a Venmo card that can be used anywhere Mastercard is accepted.

Drawbacks:

Venmo charges a 3% fee when you send money using a credit card. Also, its social aspect might not appeal to everyone.

|  |  |  |  |

Zelle

Zelle, developed by Early Warning Services, is a digital payment network backed by many major US banks. It’s like having a bank teller in your pocket. With Zelle, you can send money directly from your bank account to someone else’s bank account within minutes. It’s integrated with many banking apps, so there’s a good chance you already have access to Zelle in your existing banking app. One drawback is that Zelle doesn’t offer a protection program for authorized payments, so users need to be careful when sending money.

Key Features:

- Direct Bank Transfers: Money sent via Zelle can be transferred directly to the recipient’s bank account.

- Speed: Transactions are typically completed within minutes.

- Widespread Bank Integration: Many major banks offer Zelle within their own banking apps.

Drawbacks:

One drawback is that Zelle doesn’t offer a protection program for authorized payments, so users need to be careful when sending money.

|  |  |  |  |

Google Pay

Google Pay, developed by Google, is a digital wallet platform and online payment system. It’s like having a wallet in your Google Account. With Google Pay, you can pay in stores, on public transportation, and online, all without reaching for your wallet. You can also send and receive money directly in the app. However, Google Pay’s acceptance is not as widespread as some other payment apps, particularly outside the US.

Key Features:

- Integration with Google Services: Google Pay can be used for checkout in Google products and Android apps.

- Contactless Payments: Users can pay in stores using their phone.

- Send and Receive Money: Users can send and receive money directly in the app.

Drawbacks:

However, Google Pay’s acceptance is not as widespread as some other payment apps, particularly outside the US.

Apple Pay

Apple Pay, developed by Apple Inc., is a mobile payment and digital wallet service. It’s like having a wallet on your iPhone. With Apple Pay, you can make secure and private purchases in stores, in apps, and on the web. You can also send and receive money in Messages. However, Apple Pay is only available to Apple device users, limiting its user base.

Key Features:

- Seamless Integration with Apple Devices: Apple Pay works seamlessly with Apple devices, providing a smooth user experience.

- Security and Privacy: Apple Pay uses a method called tokenization to secure your card information.

- Contactless Payments: Users can make in-store payments using their iPhone or Apple Watch.

Drawbacks:

However, Apple Pay is only available to Apple device users, limiting its user base.

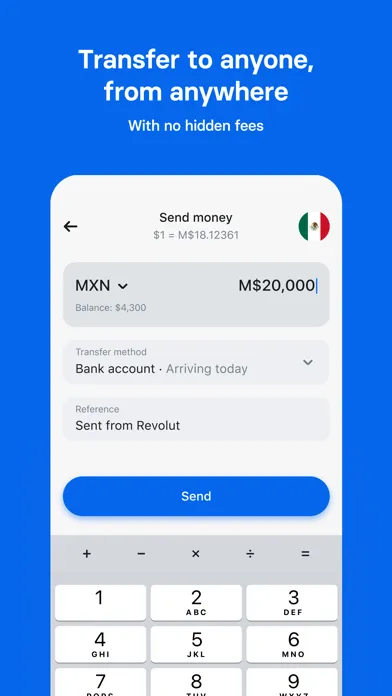

Revoult

Revolut, a British financial technology company, offers a platform that’s gaining popularity among international travelers. It’s like having a bank branch on your smartphone. With Revolut, you can send, receive, and spend money in multiple currencies with the real exchange rate. You can also set budgets, split bills, and round up payments to save money. However, some users have reported issues with account freezes, which can be inconvenient when traveling abroad.

Key Features:

- Currency Conversion: Revolut allows users toreceive, hold, and exchange 28 currencies in the app.

- Built-in Budgeting: The app includes budgeting tools that track spending and set monthly budgets.

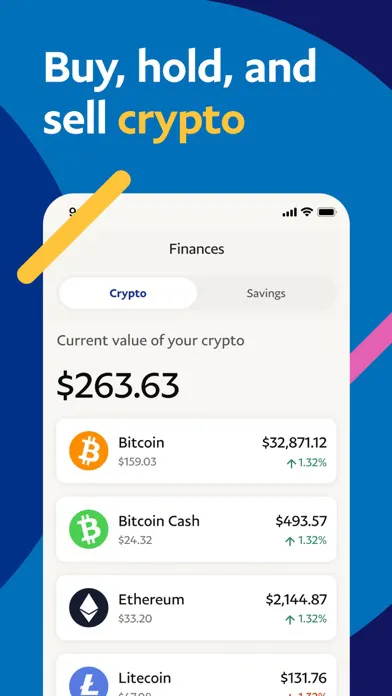

- Cryptocurrency Support: Revolut allows users to buy, hold, and sell cryptocurrencies directly in the app.

Drawbacks:

Some users have reported issues with account freezes, which can be inconvenient when traveling abroad.

|  |  |  |  |

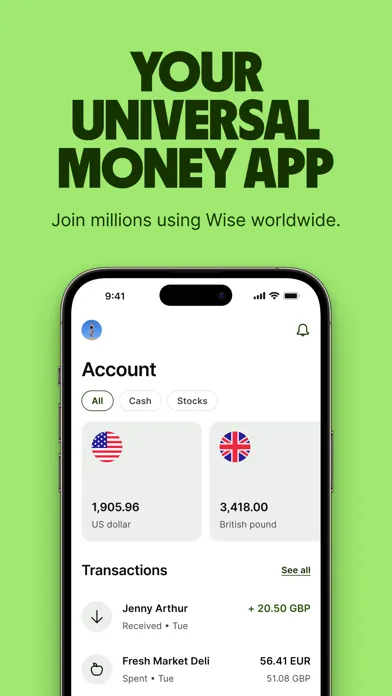

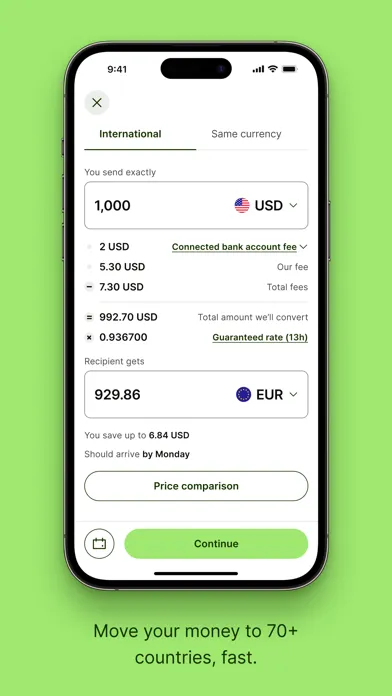

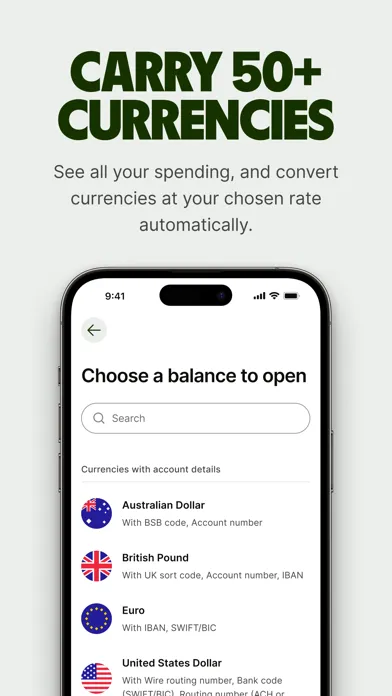

Wise (Formerly TransferWise)

Wise, developed by Wise PLC, is a platform for sending and receiving payments, mostly internationally. It’s like having a currency exchange booth in your pocket. With Wise, you can send money abroad at the real exchange rate, which is often much cheaper than what traditional banks offer. You can also hold and manage money in more than 50 currencies. This is particularly useful if you’re an expat, a freelancer with international clients, or you travel frequently. However, Wise isn’t as instant as some other apps, with transfers sometimes taking a few days.

Key Features:

- Low-Cost International Transfers: Wise uses the real exchange rate and charges a low, transparent fee.

- Multi-Currency Account: Users can hold and manage money in multiple currencies.

- Debit Card: Wise offers a debit card that can be used for payments and ATM withdrawals worldwide.

Drawbacks:

Wise isn’t as instant as some other apps, with transfers sometimes taking a few days.

|  |  |  |  |

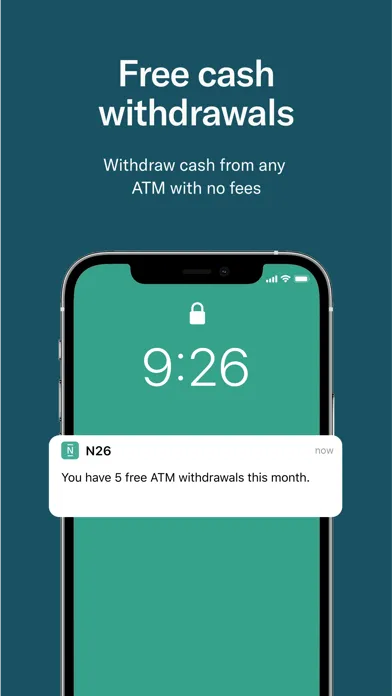

N26

N26, Europe’s most famous mobile bank, offers full control over your finances straight from your phone. It’s like having a sleek, modern bank branch in your pocket. With N26, you can make payments, set spending limits, lock or unlock your card, and receive real-time notifications for all account activity. You can also set financial goals and save money automatically with Spaces, N26’s sub-accounts. However, N26 is currently only available in Europe and the US, limiting its reach.

Key Features:

- Spaces: This feature allows users to create sub-accounts for organizing and saving money.

- Real-Time Notifications: Users receive instant notifications for all account activity.

- Free ATM Withdrawals: N26 offers free ATM withdrawals in euros.

Drawbacks:

N26 is currently only available in Europe and the US, limiting its reach.

|  |  |  |  |

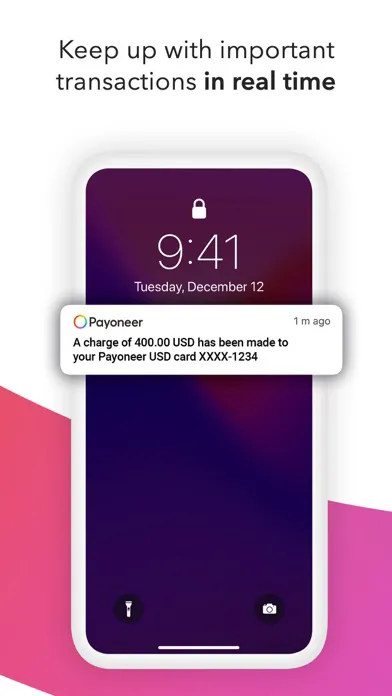

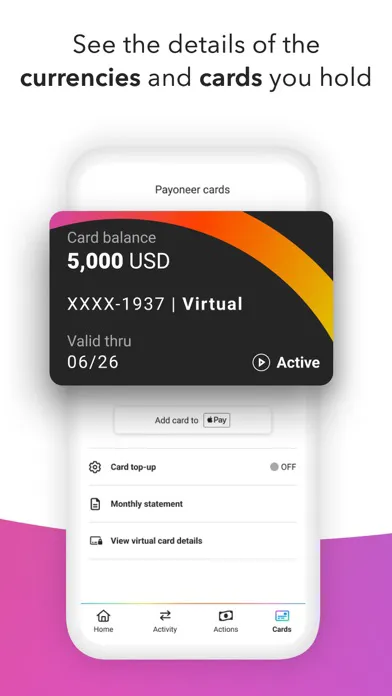

Payoneer

Payoneer, developed by Payoneer Inc., supports over 150 currencies, making it a great option for international transactions. It’s like having a global bank account. With Payoneer, you can send and receive payments locally and internationally. It’s particularly useful for freelancers, online sellers, and businesses with global clients. However, some users have reported high fees for certain types of transactions.

Key Features:

- Cross-Border Payments: Payoneer specializes in facilitating cross-border payments.

- Mass Payout Services: This feature is beneficial for businesses needing to pay multiple recipients.

- Integrated with Many Online Marketplaces: Payoneer is integrated with marketplaces like Amazon, Airbnb, and Upwork.

Drawbacks:

Some users have reported high fees for certain types of transactions.

|  |  |  |  |

Cheese

Cheese, developed by Cheese Financial, is an online bank that offers perks like cashback and early paycheck access. It’s like having a friendly, rewarding bank in your pocket. With Cheese, you can earn cash back at select stores, get a deposit bonus, and access your paycheck up to two days early. It also doesn’t charge any fees, which is a big plus. However, Cheese is a relatively new player in the market, so it may not have as many features as more established apps.

Key Features:

- No Fees: Cheese doesn’t charge monthly fees, overdraft fees, or ATM fees.

- Cashback and Bonuses: Users can earn cashback at select stores and a deposit bonus.

- Early Paycheck Access: Users can access their paychecks up to two days early.

Drawbacks:

Cheese is a relatively new player in the market, so it may not have as many features as more established apps.

|  |  |  |  |

Wrapping Up

In conclusion, while Cash App has its strengths, there are many other apps like Cash App that offer unique features and benefits. The best app for you depends on your specific needs and circumstances. We encourage you to check out these apps and share your experiences. Your insights could help others make more informed decisions. Happy banking!

Still have questions? Contact us.